Are you a contractor looking to protect your business without breaking the bank? Getting a contractor insurance quote estimate is the first step to securing the right coverage tailored to your needs.

But how do you find the best rates and make sure your policy covers all the risks unique to your trade? You’ll discover how to compare quotes from multiple carriers, understand the types of coverage you need, and get the best value for your money.

Keep reading to make sure your business stays safe and your budget stays intact.

Why Contractor Insurance Matters

Contractor insurance protects your business from many risks. It covers accidents, property damage, and legal claims. Without insurance, costs can be very high. Insurance helps pay for medical bills if someone gets hurt on the job.

Contractors often face risks like equipment theft, weather damage, and mistakes during work. Insurance also covers damage to client property. It keeps your business safe from unexpected expenses.

| Common Risks | How Insurance Helps |

|---|---|

| Injury to workers or others | Covers medical and legal costs |

| Damage to tools and equipment | Pays for repair or replacement |

| Client property damage | Protects against lawsuits |

| Work errors or accidents | Covers legal defense and claims |

Types Of Contractor Insurance

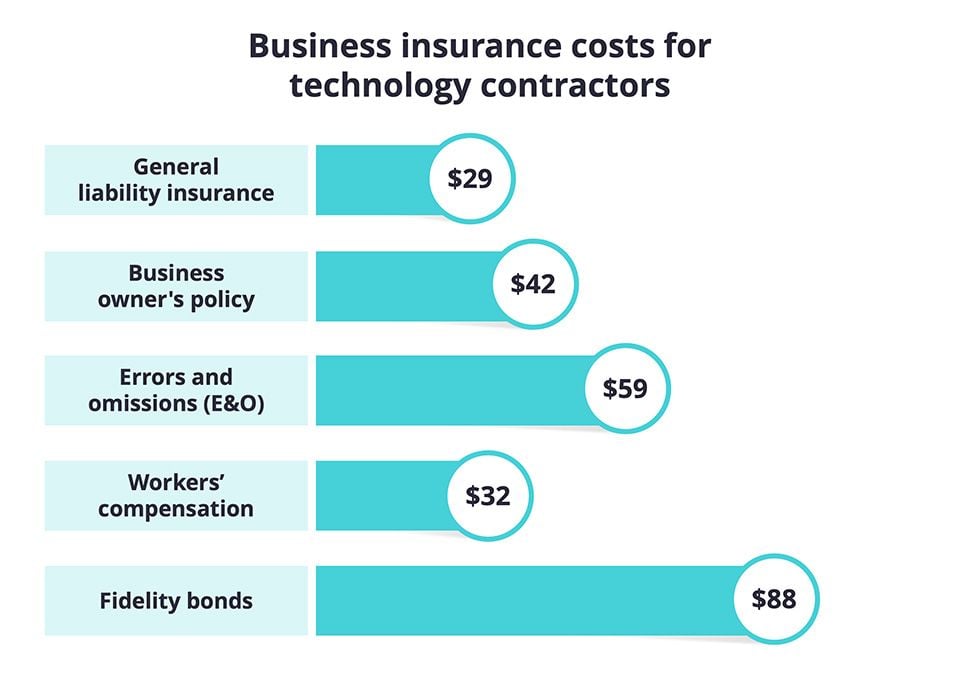

General Liability Insurance protects contractors from claims of property damage or injury. It covers accidents that happen on the job site, such as a customer slipping and falling. This insurance is essential for any contractor to avoid costly lawsuits.

Workers’ Compensation provides coverage for employees who get hurt while working. It pays for medical bills and lost wages. Most states require this insurance if you have employees.

Professional Liability covers mistakes or errors in the work done. It is also called errors and omissions insurance. This protects contractors if a client claims poor work or negligence.

Commercial Auto Insurance is for vehicles used in the business. It covers accidents, damage, or theft of work trucks and vans. Personal auto insurance usually does not cover business use.

Umbrella Policies give extra protection beyond other insurance limits. They cover large claims or lawsuits that might exceed basic coverage. This helps protect a contractor’s assets and future earnings.

Factors Affecting Insurance Quotes

Business size and revenue influence insurance quotes significantly. Larger businesses with higher revenue usually pay more. This is because they face more risks and need higher coverage.

Coverage limits and deductibles also affect the cost. Higher coverage limits mean higher premiums. Choosing a higher deductible can lower the premium but increase out-of-pocket costs when filing a claim.

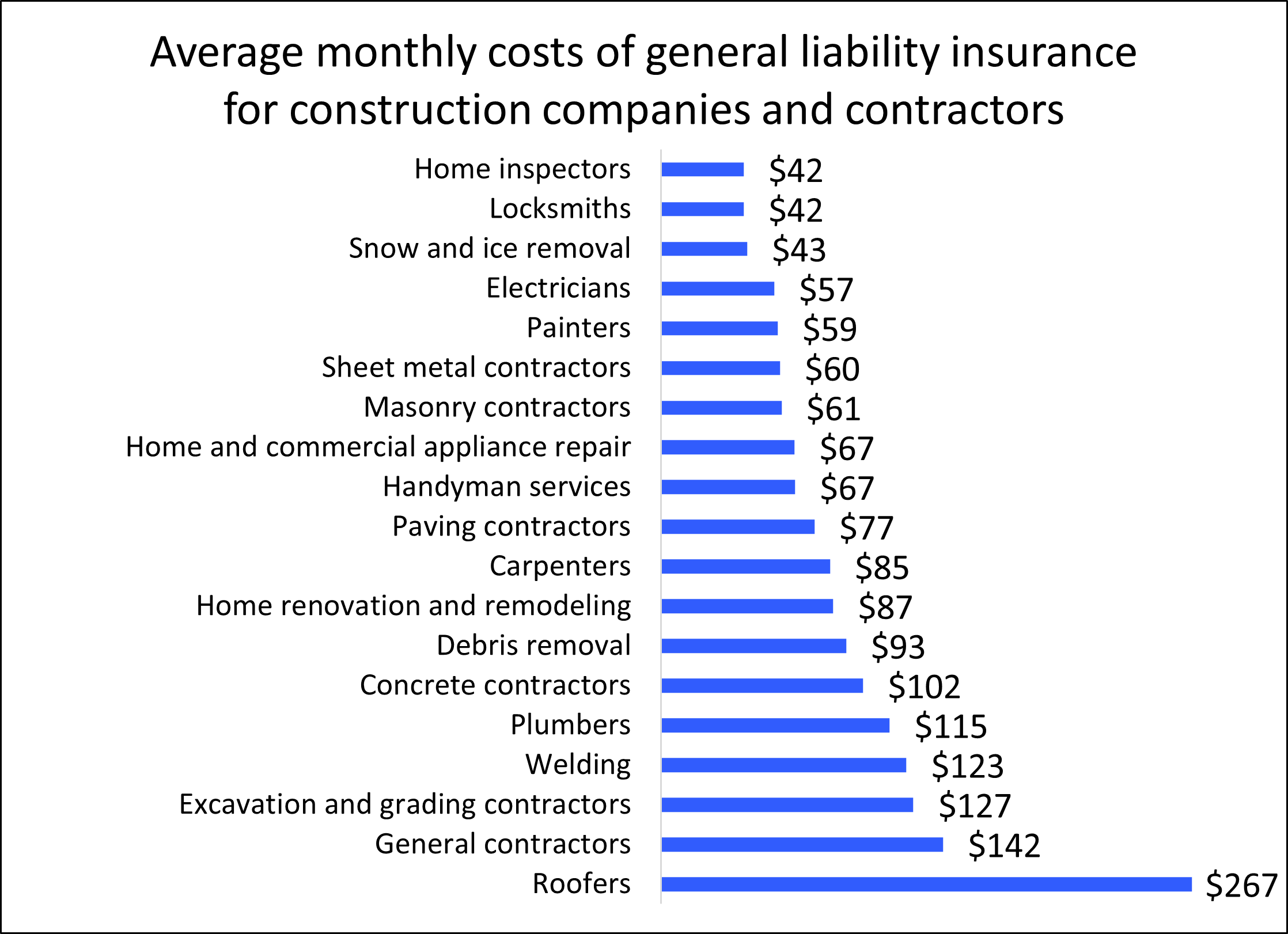

The type of contracting work matters too. Some jobs, like electrical or roofing, have higher risks. These risks lead to higher insurance costs.

Claims history impacts quotes as well. Contractors with many past claims may pay more. Insurance companies see them as higher risk.

Location and state requirements shape the insurance price. Laws and regulations vary by state. Some states require more coverage, raising the cost.

How To Get Fast Insurance Quotes

Using online quote tools helps get insurance prices quickly. Enter your details carefully to get a good estimate. These tools show prices from many insurers at once. That saves time and effort.

Working with independent agents offers personal help. They know many insurance companies well. Agents can explain options and find the best fit for your needs. They often spot discounts you might miss.

Comparing multiple carriers is key. Different companies charge different rates for the same coverage. Getting several quotes lets you find the best price and coverage. It also helps you avoid paying too much.

Always provide accurate information. Wrong details can delay your quotes or cause coverage issues later. Double-check your data like business size, location, and work type. Honest answers help insurers give precise quotes fast.

Tips For Affordable Coverage

Bundling policies can lower your overall insurance cost. Combining your contractor insurance with other policies like auto or home insurance often leads to discounts. Many insurers reward customers who buy multiple policies.

Raising deductibles means paying more out of pocket if a claim happens. This choice usually results in a lower monthly premium. Only raise deductibles if you have enough savings to cover them.

Implementing safety programs helps reduce accidents on the job. Safer workplaces lead to fewer claims and better insurance rates. Training workers and using protective gear show insurers you manage risks well.

Maintaining a clean claims record is key. Avoid filing small claims that can increase premiums later. Insurers prefer contractors with few or no past claims. A good record shows reliability and lowers costs.

Common Mistakes To Avoid

Underinsuring your business can lead to big financial problems. Not having enough coverage means you might pay out of pocket for damages or lawsuits. Always choose a policy that fits the size and risks of your work.

Ignoring state requirements puts your business at risk of fines or shutdowns. Each state has rules about the type and amount of insurance contractors must have. Check local laws before buying a policy.

Overlooking policy exclusions can cause surprises when you file a claim. Some policies do not cover certain damages or accidents. Read the fine print carefully to know what is not covered.

Using Quotes To Choose The Right Policy

Compare coverage options carefully. Choose policies that cover key risks like property damage and liability. Lower cost is good, but adequate coverage is better. Cheaper policies may leave gaps that cost more later.

Check the insurance company’s reputation. Look for reviews and ratings from other contractors. A reliable carrier pays claims quickly and offers good customer service. Avoid carriers with many complaints.

Read the policy terms thoroughly. Understand what is included and excluded. Check limits, deductibles, and any additional fees. Make sure the policy fits your specific contracting work.

Frequently Asked Questions

How Much Should Contractor Insurance Cost?

Contractor insurance typically costs between $400 and $7,000 annually, depending on coverage, location, and business size.

How Much Does A $1,000,000 Liability Insurance Policy Cost?

A $1,000,000 liability insurance policy typically costs between $400 and $1,500 annually. Rates vary by industry, location, and coverage specifics.

What Not To Tell Your Contractor?

Avoid sharing your maximum budget, personal financial details, or plans to hire unlicensed workers. Don’t reveal dissatisfaction with previous contractors. Keep project changes and deadlines vague until finalized.

What’s The Best Insurance For Contractors?

The best insurance for contractors includes general liability, workers’ compensation, and commercial auto coverage. Choose policies that fit your trade and risks. Compare multiple carriers for competitive rates and tailored protection.

Conclusion

Getting a contractor insurance quote estimate helps protect your business. It allows you to compare costs and coverage options easily. Choosing the right insurance saves money and reduces risks. Many insurers offer tailored plans for contractors in Austin, Texas. Quick quotes let you make informed decisions fast.

Protect your work, tools, and clients with proper coverage. Start with a few quotes to find the best fit. Insurance keeps your business safe and ready for challenges ahead.

Read More

- Business Liability Quote Online: Get Instant, Affordable Coverage Today

- Condo Insurance Quote Comparison: Save Big with Smart Choices

- Free Policy Quote Estimate: Unlock Savings with No Hassle!

- Best Premium Quote Comparison: Unlock Top Savings Today

- Commercial Insurance Quote Comparison: Find the Best Deals Fast

- Professional Indemnity Quote: Get Accurate, Fast, and Affordable Today

- Classic Auto Quote Estimate: Get Accurate, Fast & Free Today!

- Landlord Insurance Quote Online: Quick, Affordable Coverage Today

- Same Day Insurance Quote: Get Instant Coverage Today!

- Commercial Fleet Quote Comparison: Save Big with Smart Choices